This is an excerpt from the 0xResearch newsletter. To access the full editions, subscribe.

We often refer to this sector as the “blockchain” industry, but there is a growing sentiment of fatigue towards the proliferation of new chains.

Launching a new blockchain in 2025 is likely to face significant skepticism on platforms like Twitter. This skepticism was evident in the recent flurry of L1 blockchain fundraises.

- Camp Network, a L1 focused on intellectual property, raised $30 million at a valuation of $400 million.

- Unto, a L1 based on SVM technology, raised $14.4 million at a valuation of $140 million.

- Miden, a zk rollup, raised $25 million (valuation undisclosed).

The question on everyone’s mind is, “Why another chain?” The simplest explanation seems to be the pursuit of profit, also known as the L1 premium!

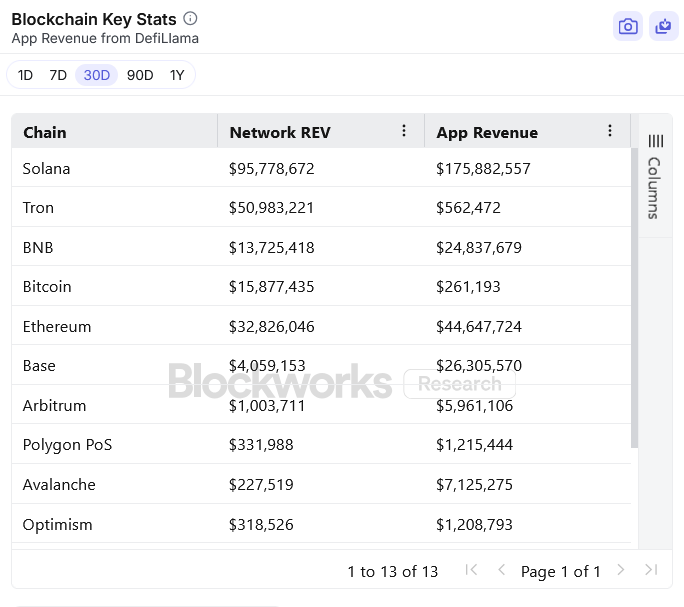

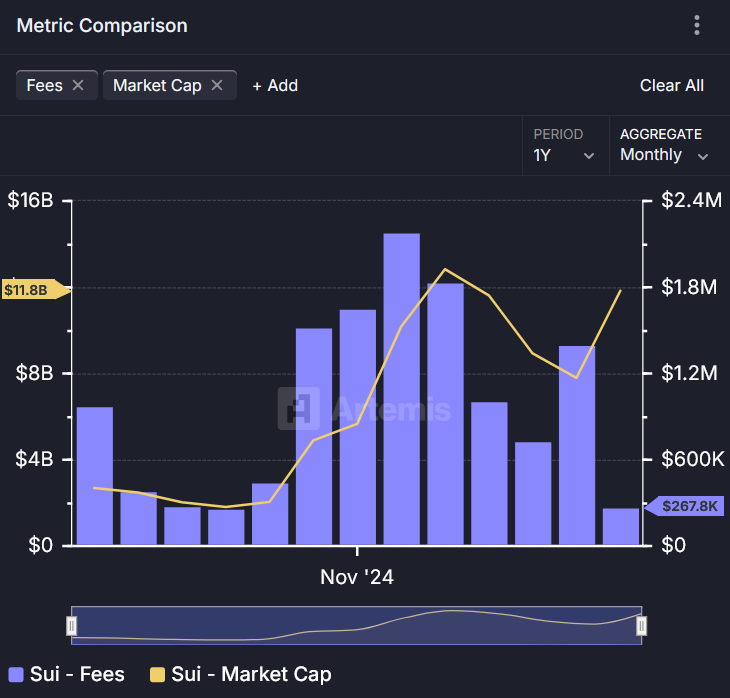

For instance, the recent price surge of SUI raises eyebrows — how can a token with a market cap of $6.8 billion nearly double in value within two weeks?

It’s clear that this price surge is not driven by fundamental factors, especially considering the low fees generated on SUI compared to its peak in December.

While SUI may be an outlier, the allure of the L1 premium still persists, albeit waning.

Despite the skepticism, the incentive to launch new L1s remains strong.

Another explanation for the continuous influx of new chains is the differing visions that founders have regarding the optimization of a blockchain.

Decisions on the design of the execution environment, MEV capture, data availability layer, and the use of standardized oracles and gas tokens are crucial and can significantly impact the long-term success of a chain.

Getting all protocol builders to reach a consensus is akin to trying to agree on a buffet menu with a hundred people.

Moreover, there are social considerations at play. For example, Rogue, an upcoming zk rollup by @fede_intern, aims for a fair launch without VCs or insider allocations, inspired by Bitcoin’s ethos.

Differing opinions among builders lead to the creation of new chains — a manifestation of economic freedom that should be celebrated.

A Potential Solution?

There is some solace in the fact that L1 valuations are beginning to normalize.

Consider Monad, rumored to have reached unicorn status with a valuation in the billion-dollar range according to Pitchbook, and Initia L1, valued at $350 million last year.

These figures are a far cry from the exorbitant valuations seen in the previous cycle.

Public and private markets are both showing signs of correction, indicating that the market is responding to the oversaturation of new chains.

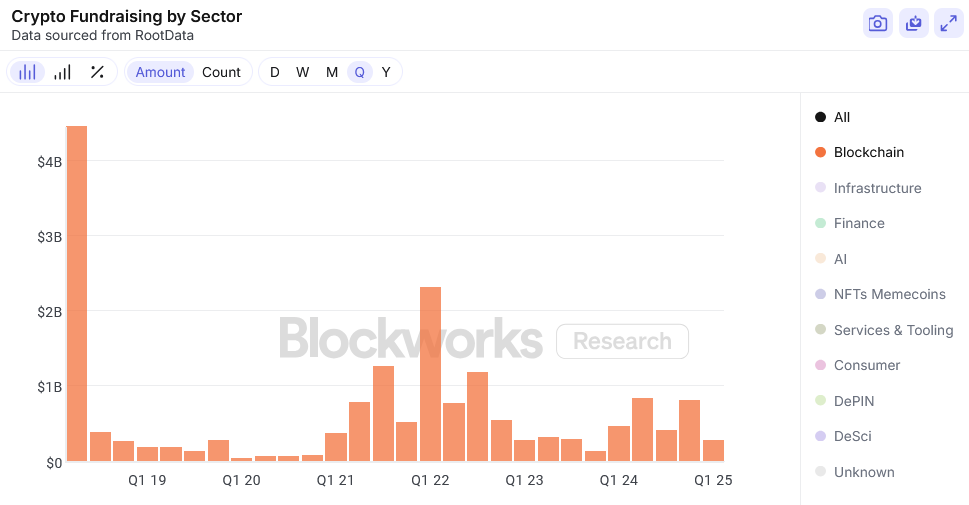

When viewed from a broader perspective, the total funding raised for blockchains is on a downward trend, as illustrated in the chart below.

For those weary of the abundance of chains or those advocating for a chain-less future, this trend may not be entirely satisfactory.

There is also a growing desire to see more applications developed within the blockchain ecosystem.

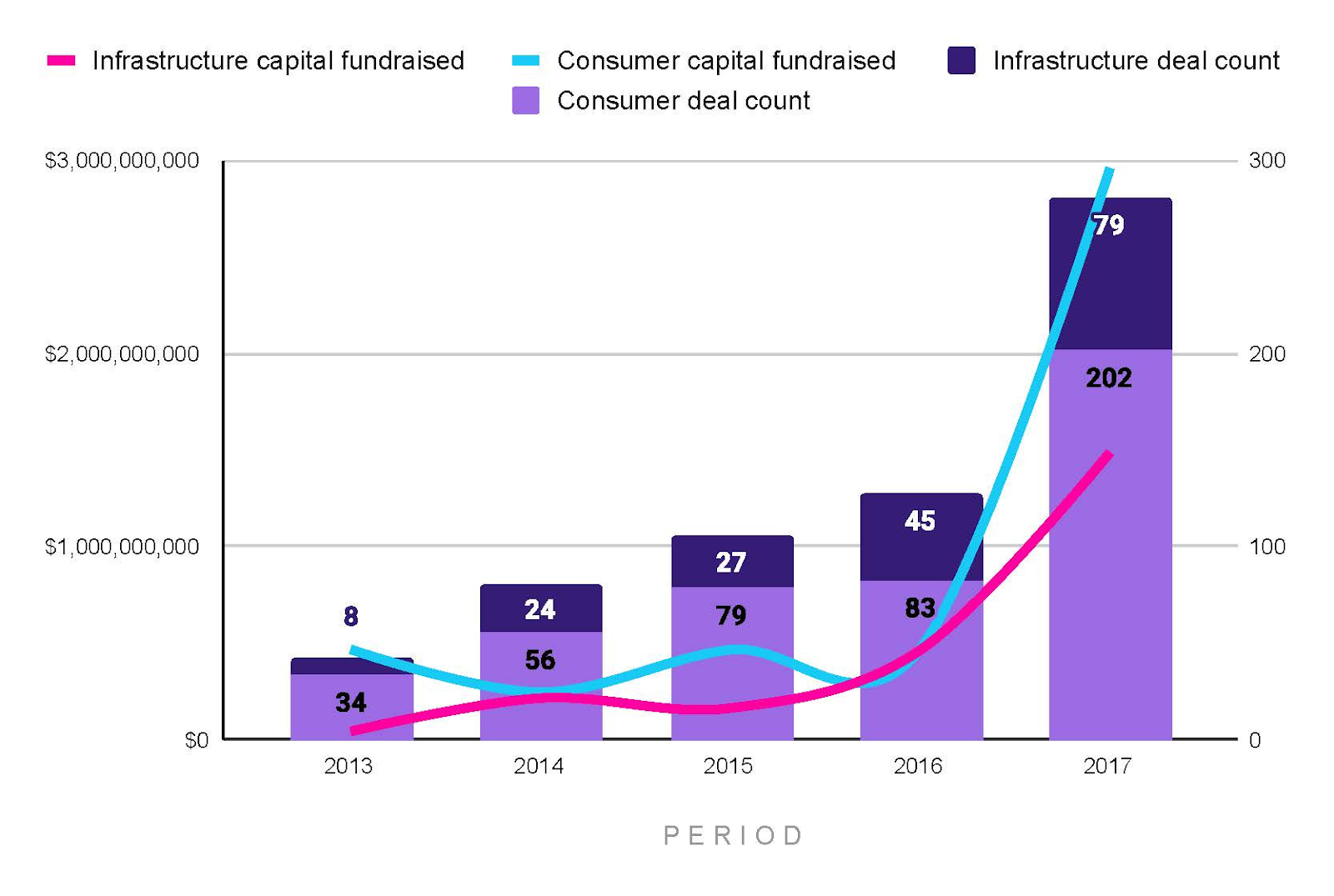

Interestingly, consumer apps received more venture funding compared to infrastructure projects between 2013-2017, a trend that has since reversed.

Source: Outlier Ventures

Why have VCs shifted their focus away from application funding? According to 1kx, a prominent investor in consumer apps, applications rely on immediate traction and follow-through for success, creating a different investment dynamic compared to infrastructure projects.